Housing Affordability Part 2

/

Property investors who purchased "off the plan" in 2014 or 2015 may run into serious problems completing their purchases when construction finishes later this year.

Read MoreOur commentary on issues important to home owners, investors and borrowers

Property investors who purchased "off the plan" in 2014 or 2015 may run into serious problems completing their purchases when construction finishes later this year.

Read MoreLatest Residex Property Market Report for NSW shows that prices have peaked. We summarise what's in store for the coming year.

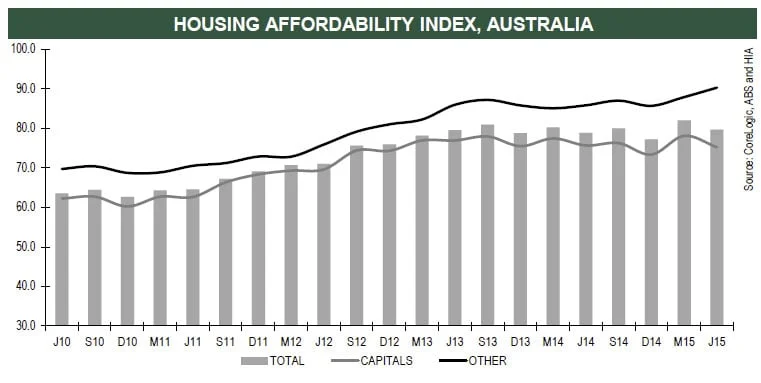

Read MoreWhich way for property prices this year? This is driven in part by housing affordability. But what do we mean by affordability and how do we best measure it? To my mind there are several ways of looking at housing affordability:

House prices versus average incomes

Proportion of household income needed to purchase an average property

Average weekly rent versus average incomes

Each of these methodologies tells a different story.

Read MoreOur privacy policy has been updated. To read it please go here.

Today, one of the institutions that we could most liken to a community bank has seen fit to raise its interest rates in response to recent chnages announced by the big banks. We look into the reasons behind this decision and its potential impact on the home loan market.

Read MoreAnother major lender announces an across the board interest rate increase for existing home loan customers - coincidentally to take effect on the same day as Westpac's signalled rate cut in November.

Read MoreLoanscape is your information resource about lending and property.

Loanscape has today released its Borrowing Capacity Index for Q3/2024. It shows that the borrowing capacities of Australian individuals and families have started to recover after the sharp decline over the past 2 years. Lower income borrowers continue to be disproportionately impacted by interest rate increases: the family income required to qualify for the average size loan in Australia is 37% higher than 2 years ago.

Loanscape has today released its Borrowing Capacity Index for Q2/2024. It shows that the borrowing capacities of Australian individuals and families have stabilised after the sharp decline over the past 2 years. Lower income borrowers continue to be disproportionately impacted by interest rate increases: the family income required to qualify for the average size loan in Australia is 35% higher than 2 years ago.

Combined dwelling values have re-accelerated across the nation in February, with all mainland capitals soaring in value. It probably comes as no surprise that Perth claimed the top spot by gaining a whopping 1.8% for the month

Loanscape has today released its Borrowing Capacity Index for Q1/2024. It shows that the borrowing capacities of Australian individuals and families continue to decline. The more modest decline in the size of average loans being taken confirms that lower income borrowers are being disproportionately impacted by interest rate hikes: the family income required to qualify for the average loan in Australia is now 32% higher than 18 months ago.

The end of the year is fast approaching, with most capitals experiencing a strong recovery on dwelling values from the downturn that culminated at the start of 2023.

The recovery is mainly due to an influx of immigration and constricted supply, which the Government is trying to remedy with its ambitious goal of building 1.2 million homes by 2029 through HAFF.

Loanscape has today released its Borrowing Capacity Index for Q4/2024. It confirms the forecast trend that borrowing capacities of Australian individuals and families are recovering from their low levels which coincided with the last of the recent increases to borrowing rates initiated by the Reserve Bank of Australia.